A licensed agent with a clean record and a current compliance certificate sits across from a worried customer. The customer asks a simple question: will this policy cover water damage in the basement. The agent, wanting to close and fairly sure the answer is yes, says that it will. It does not, at least not the way this customer means it. Eight months later a pipe bursts, the claim is denied, and the agent is named in a complaint for misrepresenting coverage. Nobody set out to break a rule. The rule broke in a single sentence, in the middle of an ordinary conversation.

That is what almost every insurance compliance violation looks like up close. The agent knew the rule and passed the module, and then, under the normal pressure of a live conversation, they said the wrong thing. Compliance training that only checks whether an agent can recall a rule never rehearses the moment the rule actually breaks, and it falls out of date the day a regulator changes a requirement. What follows is a field guide to the moments where agents really slip, drawn from what state insurance departments cite most often, and how to drill each one so the compliant response holds under pressure.

The pattern behind every violation regulators cite

Read through the enforcement pages of any state insurance department and a pattern jumps out. The violations that get agents fined are almost never failures of knowledge. They are failures of behavior in a specific conversation.

Regulators examine the conversation, not the certificate

When a state opens a market conduct examination, it does not ask to see completion certificates. It reviews advertising, claims handling, disclosures, and whether the products sold were suitable, which is to say it examines what agents actually said and did with customers. The Pennsylvania Insurance Department describes market conduct exams as reviews of claims handling, complaints, marketing, and suitability, and the outcome can be fines, restitution, or a suspended license. A completion certificate is no defense in that room, because the examiner is looking at the conversation, not the coursework.

The compliance case files: where agents actually slip

These are the moments state regulators cite most, each a behavior under pressure rather than a fact to memorize, and each one that can be drilled through AI sales training until the compliant response is automatic.

1. Misstating what a policy covers

The most common trap is answering a coverage question with a confident yes to keep the sale moving. An agent leads a customer to believe they are covered for something the policy excludes, and that single sentence becomes a material misrepresentation the moment a claim is denied. The allegations Florida investigates include exactly this, statements about coverage that turn out to be untrue or misleading. The drill is a roleplay where the customer asks pointed coverage questions and fishes for a reassuring overstatement, scored on whether the agent states coverage accurately and names the exclusions out loud.

2. Recommending an unsuitable product

The second trap is steering a customer toward the product that pays the agent more rather than the one that fits. It shows up as unnecessary replacement of a life or annuity policy, or an indexed product sold on growth projections that quietly ignore fees and caps. The California Department of Insurance flags unsuitable replacement of policies, especially for seniors, as a recurring form of producer misconduct. The drill is a roleplay where the suitable recommendation earns the smaller commission, scored on whether the agent recommends what fits and documents why.

3. Skipping or rushing a required disclosure

The third trap is triggered by an impatient customer. The client wants to move fast, so the agent speeds through or skips a mandated disclosure to keep them happy, which is itself the violation. Regulators treat missing or misleading disclosures and unapproved sales language as deceptive practice, regardless of intent. The drill is a roleplay with a customer who acts rushed and irritated by the details, scored on whether the agent delivers the full disclosure anyway, at the customer's pace or not.

4. Promising that a claim will be paid

The fourth trap is the reassurance an anxious buyer is begging for. The customer asks whether the policy will definitely pay out if something happens, and the agent, wanting to comfort them and close, says yes. Guaranteeing a claim outcome misstates how coverage works and creates both a misrepresentation and a bad-faith exposure. The drill is a sales roleplay with a nervous buyer who keeps pushing for guarantees, scored on whether the agent stays honest about what is and is not covered without promising an outcome.

5. Crossing the line on Medicare and health

The fifth trap is specific to health and senior markets, where the rules are strictest. An agent drifts outside the plans a Medicare client agreed to discuss, or oversimplifies coverage in a way that misleads, both of which violate CMS marketing rules. The California Department of Insurance lists deceptive sale of Medicare Advantage and prescription drug plans among the schemes it investigates. The drill is a roleplay scenario with a confused senior, scored on whether the agent respects scope-of-appointment limits and explains options accurately and plainly.

Why the rulebook never stops moving

Even a team that has drilled every case file has a second problem, because the rules underneath those drills keep changing.

1. The requirements change every year

Insurance rules are a moving target. State departments update continuing education, ethics, and cybersecurity requirements, and health work moves fastest of all, with CMS requiring agents and brokers to complete fresh Marketplace registration and training every plan year. A static annual module reflects last year's rules, and rebuilding and redistributing it takes weeks a team rarely has, so agents keep practicing requirements that have already changed.

2. A violation in one state follows you everywhere

The stakes of falling behind are higher than they look, because a disciplinary action does not stay local. The NAIC maintains a cross-state system that tracks regulatory actions against producers, and a suspension or revocation in one state is grounds for discipline in every other state where an agent holds a license. Keeping a multi-state team current is therefore not housekeeping, it is protection of the whole book, and it demands training that can be refreshed the moment any one jurisdiction moves.

Turning the case files into drills

Knowing where agents slip is only useful if the practice actually changes behavior, which is where the training method matters.

1. Score the moment, not the module

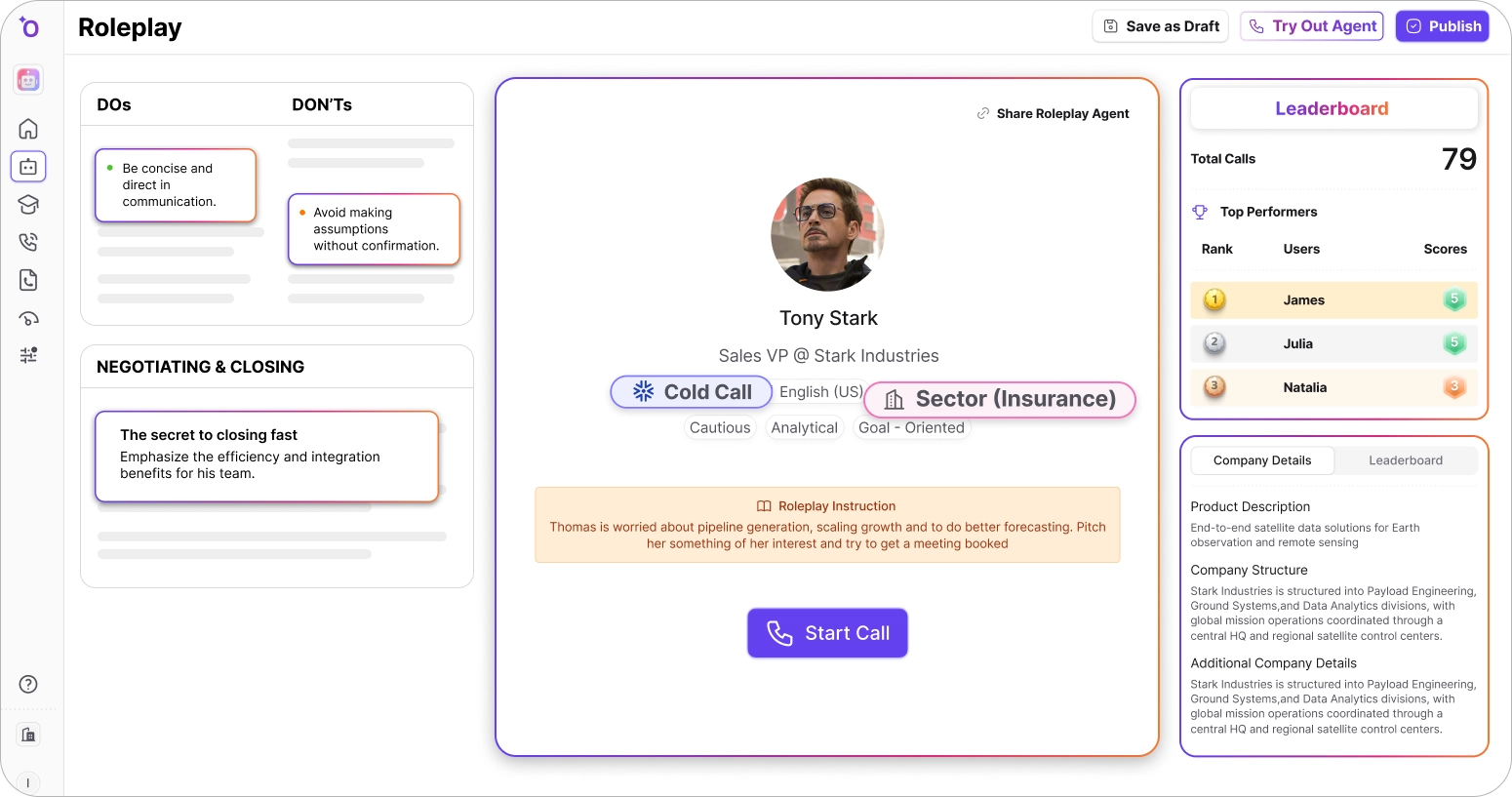

A quiz measures recall, but the case files above are behaviors, so they have to be practiced as behaviors. In an AI roleplay, an agent handles the risky conversation and the system scores whether they stayed compliant, flagging the promised claim, the skipped disclosure, or the unsuitable recommendation the instant it happens. Every session is recorded and scored, which turns training into the kind of evidence a market conduct examiner actually wants, a demonstration of compliant behavior rather than a completion checkbox. Research summarized by eLearning Industry on the forgetting curve shows knowledge fades within days without this kind of repetition.

2. A drill for the highest-risk moment

Here is a ready-to-run drill for the coverage-misstatement case file, the one that produces the most complaints. Paste it into an AI roleplay tool, and it plays the customer while scoring the agent.

How Outdoo AI keeps insurance teams compliant

Outdoo AI is the enterprise AI roleplay and coaching platform built to turn these case files into a trained, measurable, and current skill.

1. Score compliant behavior on every call

Agents practice the risky conversations in chat, voice, and video, and every session is graded on a scorecard you build around your compliance rules, so accurate coverage statements, complete disclosures, and suitable recommendations become scored requirements rather than hopes. The platform flags the exact moment an agent oversteps and lets them re-drill it until the compliant response is automatic.

2. Refresh the drills the day a rule changes

When a state or CMS updates a requirement, a scenario and its scoring can be refreshed and pushed to the whole team in the languages they sell in, so agents drill the current rule rather than last year's. Practice packages into courses with certification gates, and completion exports to your learning system through SCORM for the records compliance teams have to keep.

3. Protect the data the training runs on

Because this is a regulated industry, the platform has to protect the data it trains on. Outdoo AI maintains SOC 2 Type 2, GDPR, HIPAA, and CCPA compliance with PII scrubbing, which makes it safe to build scenarios from real client and health-related calls without trading a training problem for a privacy one.

Where to start - Pick the case file your team fails most

Do not try to fix every compliance risk at once. Pull your recent complaints and find the one case file your team slips on most, whether that is a misstated coverage answer, an unsuitable recommendation, or a skipped disclosure, and build a scored roleplay for exactly that moment. Drill it weekly, refresh it when the rule changes, and keep the scored records. Schedule a demo to see how Outdoo AI keeps your insurance team compliant and current as the rules keep moving.

Frequently Asked Questions

.svg)

Compliance training teaches agents to follow the laws governing selling and servicing policies: licensing, continuing education, accurate disclosures, suitability, market conduct, data privacy, and anti-money-laundering rules set by state departments, the NAIC, and federal regulators like CMS.

Most violations are not failures of knowledge but failures of behavior in a live conversation. A well-trained agent, under pressure to help or close, misstates coverage, skips a disclosure, or promises a claim. The knowledge was there but the compliant response did not hold in the moment.

When a state or federal rule changes, a roleplay scenario and its scoring can be refreshed and pushed to the team immediately, so agents re-drill the new requirement the same week. That replaces the slow cycle of rebuilding a static course.

The moments state regulators cite most: misstating what a policy covers, recommending an unsuitable product, skipping or rushing a required disclosure, promising a claim will be paid, and crossing Medicare scope and marketing rules.

Outdoo AI lets agents practice the risky conversations where violations happen and scores whether they stay compliant, flagging misstated coverage, skipped disclosures, and unsuitable recommendations. Scenarios refresh the day a rule changes, with SOC 2 Type 2 and HIPAA data protection.