Insurance is one of the hardest products in the world to sell, because the agent is not really selling a policy. They are selling trust, in a conversation loaded with fear, money, and skepticism, governed by regulations that punish a careless sentence. An agent can know every product detail and still freeze when a grieving widow questions a premium, or fold when a price-shopper waves a cheaper online quote. That gap between knowing the product and handling the moment is not a knowledge problem. It is a practice problem, and it is exactly what roleplay is built to solve.

This is a detailed library of AI roleplay scenarios for insurance sales teams, organized into the three pillars that decide most policies: discovery, objection handling, and closing. For each scenario you get the setup, the challenge that makes it hard, a sample script for the moment of truth, the skills it builds, a coaching takeaway, and a compliance note where the conversation touches regulated ground. You also get a scorecard, ready-to-copy prompts, the compliance guardrails insurance practice demands, and how Outdoo AI runs it across an agency or carrier at scale.

Why insurance sales teams need roleplay more than most teams

Insurance carries a combination of pressures that few other sales jobs do, and each one raises the value of practice.

1. The conversation is emotional before it is transactional

Insurance touches the things people least want to think about: death, disability, illness, and the loss of a home. Customers arrive anxious, defensive, or grieving, and an agent who leads with product features instead of empathy loses them in the first minute. Roleplay lets agents practice reading and responding to emotion, which is a skill no product manual teaches and no one masters by watching a webinar.

2. Trust is low and skepticism is earned

Many prospects approach insurance already suspicious, often after a bad claim experience of their own or a story from a friend. An agent has to acknowledge that skepticism without getting defensive and rebuild trust before any product talk lands. Practicing those trust-repair moments matters more in insurance than almost anywhere else, because the customer is looking for a reason to say no.

3. Every sentence is a compliance decision

Insurance is heavily regulated, and a single careless promise about a claim or a misstatement about coverage can create a regulatory problem and a broken trust. Agents have to sell persuasively while staying inside suitability rules, disclosure requirements, and product regulations that vary by state and line. Roleplay is the only safe place to practice compliant language under pressure before it happens on a live, recorded call. Research summarized byeLearning Industry on the forgetting curve shows that without reinforcement, most training fades within days, so a one-time compliance webinar does not build the reflex a live call demands.

How to build an insurance sales roleplay that actually works

A roleplay only builds insurance skill if it mirrors the real customer, the real objections, and the real compliance line. Four setup choices make that happen.

1. Match the persona to the product line and customer

A Medicare prospect, a young parent buying term life, and a small business owner shopping commercial coverage are three completely different conversations. Build personas that match your actual book, with the communication style, budget sensitivity, and concerns of each segment, so the practice transfers to the calls agents really take.

2. Pull objections from your real calls, not a generic list

The objections that stump your team are specific. Mine your recorded calls and ask your top performers what made a new agent freeze last week, then build those exact objections into the roleplay. A buyer who folds after one reframe teaches nothing, so configure the AI prospect to push the way a real one does.

3. Build the compliance line into the scenario

Insurance roleplay should reward compliant persuasion and flag the moments an agent oversteps, such as promising a claim will be paid or describing coverage inaccurately. Bake the regulatory guardrails into the scenario and the scorecard, so agents practice selling and staying compliant at the same time, because on a live call those are not two separate skills.

4. Score every session on an insurance-specific rubric

Generic sales scorecards miss what matters in insurance. Score needs-discovery depth, emotional read, plain-language explanation, compliant accuracy, value-over-price framing, and the close, so the score reflects what actually earns and keeps a policyholder.

Discovery scenarios: needs analysis that earns the recommendation

Discovery in insurance is needs analysis, and it is what separates genuine advising from product pushing. These scenarios build the consultative questioning that makes every later recommendation credible.

1. Life insurance needs analysis for new parents

Setup: A couple just had their first child and reached out about life insurance, but they have no idea how much they need or which type fits.

The challenge: Run a full needs analysis, income replacement, debts, future education costs, and existing coverage, without overwhelming two sleep-deprived new parents or jumping to a quote.

Sample script:

Congratulations on the new arrival. Before I mention any policy, I want to understand what you would want protected if something happened to either of you. Can you walk me through your monthly income, any debts like a mortgage, and what you would hope to provide for your child down the road?

Skills practiced: needs analysis, active listening, empathy, consultative questioning.

Coaching takeaway: Practice resisting the urge to quote before the need is fully mapped. The recommendation only lands if the customer feels understood first.

Compliance note: The recommendation must be suitable to the documented need, so the discovery is not just rapport, it is the record that justifies what you sell.

2. Medicare discovery with a confused, over-marketed senior

Setup: A 66-year-old recently retired and is being bombarded with Medicare calls. They are confused about their options and frustrated by aggressive marketing.

The challenge: Slow the conversation down, build trust, and clarify their real situation, current doctors, prescriptions, and budget, without adding to the overwhelm, using a pace and vocabulary that fit a senior.

Sample script:

I know you have probably had a dozen calls this week, so I will keep this simple and go at your pace. To point you in the right direction, can you tell me which doctors you want to keep seeing and which prescriptions you take regularly?

Skills practiced: senior communication, pacing, plain language, trust-building.

Coaching takeaway: Practice matching the customer's pace and stripping out jargon. With seniors, slowing down is a closing skill.

Compliance note: Medicare sales are tightly regulated, including scope-of-appointment and disclosure rules, so the roleplay should reinforce the required steps rather than skip past them.

3. Commercial and P&C risk discovery for a small business owner

Setup: A small business owner is shopping for commercial coverage and is focused entirely on price, unaware of their actual risk exposure.

The challenge: Uncover the real risk profile, property, liability, business interruption, and employees, and shift the conversation from price to risk before any quote.

Sample script:

Before we talk numbers, help me understand the business so I do not accidentally under-insure you. What would happen to your revenue if you had to close for two weeks after a fire, and do you have anyone working for you?

Skills practiced: risk discovery, value-over-price framing, business acumen.

Coaching takeaway: Practice quantifying the cost of being underinsured, because that is what moves a price-focused buyer to a coverage conversation.

Objection-handling scenarios: the heart of insurance sales

Customers rarely say yes the first time. They hesitate, push back, and test, and the agent who handles those moments calmly is the one who closes. These are the objection scenarios worth drilling until the responses become automatic.

1. The premium is too expensive

Setup: After a strong needs presentation, the prospect balks at the monthly premium.

The challenge: Reframe cost as protection against a far larger financial risk without dismissing the budget concern, and diagnose whether the issue is true affordability or perceived value.

Sample script:

I hear you, and I never want to put you in a policy you cannot sustain. Can I ask, is the concern the monthly number itself, or whether the coverage is worth it? If it is the number, we have options on coverage levels, and if it is the value, let me show you exactly what this protects against.

Skills practiced: value reframing, objection diagnosis, empathy, tone control.

Coaching takeaway: Practice diagnosing before adjusting. Cutting coverage to hit a price is the lazy move, and it often leaves the customer underinsured.

Compliance note: Any coverage adjustment must still be suitable, so agents should not strip protection below the documented need just to win the sale.

2. I already have coverage

Setup: The prospect says they already have insurance and sees no reason to keep talking.

The challenge: Earn the right to a coverage review without attacking their current agent or policy, and surface the gaps they do not know about.

Sample script:

That is good to hear, and I am not here to replace something that works for you. Most people I review are surprised by one or two gaps, like coverage that has not kept up with a new mortgage or a new child. Would a quick second look be worth it, even just to confirm you are set?

Skills practiced: non-confrontational positioning, gap discovery, humility.

Coaching takeaway: Practice the second-look frame. The goal is a review, not a teardown of the incumbent.

Compliance note: Agents must not disparage a competitor or misrepresent the prospect's existing policy to create doubt.

3. I will just buy the cheapest policy online

Setup: A price-shopper says they can get coverage cheaper online and asks why they even need an agent.

The challenge: Differentiate on advice, claims advocacy, and the risk of being underinsured, without badmouthing direct channels.

Sample script:

You absolutely can, and for some people that works fine. The difference usually shows up at claim time. A bare-bones online policy often leaves out the coverage you would actually need, and there is no one in your corner when you file. Can I show you what those cheaper policies typically leave out?

Skills practiced: value differentiation, claims-advocacy framing, cost-of-gap.

Coaching takeaway: Practice the claim-time framing, which is where the value of advice becomes concrete.

Compliance note: Do not promise specific claim outcomes. Speak to coverage differences accurately rather than guaranteeing what a carrier will pay.

4. I need to think about it

Setup: At the end of an otherwise strong conversation, the prospect stalls with a vague I need to think about it.

The challenge: Surface the real hesitation instead of accepting the stall, and create gentle, honest urgency tied to real factors.

Sample script:

Totally fair, this is an important decision. So I can actually be useful while you think it over, what is the one thing you are still unsure about, the coverage amount, the cost, or whether now is the right time?

Skills practiced: stall diagnosis, gentle urgency, securing a next step.

Coaching takeaway: Practice converting a vague stall into a specific, answerable concern, because you cannot resolve what the customer will not name.

5. The rate-increase objection at renewal

Setup: An existing policyholder calls upset about a premium increase at renewal and is threatening to leave.

The challenge: Acknowledge the frustration, explain the increase honestly, and re-anchor on value and options before they shop the policy away.

Sample script:

I completely understand the frustration, and I want to be straight with you about what drove the increase. Before you shop around, let me walk you through what your policy now covers and a couple of options that could bring the number down without leaving you exposed.

Skills practiced: retention, transparency, de-escalation, value re-anchoring.

Coaching takeaway: Practice leading with empathy and an honest explanation. Retention is won or lost in the first thirty seconds of this call.

Compliance note: Explain the reasons for an increase accurately, and never misstate what drove it.

6. I do not trust insurance companies

Setup: A skeptical prospect with a past bad claim experience makes it clear they do not trust the industry.

The challenge: Acknowledge the distrust openly, demonstrate transparency and advocacy, and rebuild enough trust to continue, all before any product talk.

Sample script:

I get it, and honestly a lot of that skepticism is earned. So let me be different in one concrete way. I will show you exactly what is covered and what is not, in plain language, before you decide anything. If I ever oversell you, you will know it. Does that feel fair?

Skills practiced: trust repair, transparency, emotional intelligence.

Coaching takeaway: Practice acknowledging distrust without becoming defensive, which is the instinct that kills these conversations.

Compliance note: Transparency about exclusions is both the trust-building move and the compliant one, so this scenario trains both at once.

Closing scenarios: asking for the business with confidence

A great needs analysis and clean objection handling still lose the deal if the agent cannot ask for the business. These scenarios build the confident, compliant close.

1. The assumptive, one-call close

Setup: The needs match is strong and the prospect is warm. It is time to ask for the business.

The challenge: Move to the close confidently with an assumptive question rather than a weak so what do you think, and give a clear next step.

Sample script:

Based on everything you have shared, the level we discussed protects your family the way you described wanting. Would you prefer monthly or quarterly billing, and should we set the start date for the first of next month?

Skills practiced: assumptive close, confidence, next-step clarity.

Coaching takeaway: Practice replacing tentative language with a confident assumptive close. Hesitation in the agent invites hesitation in the customer.

2. The procrastinator and honest urgency

Setup: A qualified prospect keeps delaying with maybe next year, even though the need is real and they reached out themselves.

The challenge: Create honest urgency tied to real factors, age-based premium increases, current health, and the life event that prompted the inquiry, without manufacturing fear.

Sample script:

I never want to pressure you, but I do want you to have the facts. The premium is based on your age and health today, and both only move in one direction. The protection you wanted for your family is either in place if something happens, or it is not. What would make it easier to move forward this month?

Skills practiced: honest urgency, reframing the cost of delay, closing.

Coaching takeaway: Practice urgency that is truthful rather than manufactured, because false pressure is both a trust killer and a compliance risk.

Compliance note: Urgency must rest on accurate facts such as real rate and health factors, not fabricated deadlines or scare tactics.

3. The bundling and cross-sell close

Setup: A satisfied auto client is on the line, and there is a clear opportunity to bundle home coverage or add life.

The challenge: Position the cross-sell as a benefit, a discount and a closed coverage gap, rather than a quota grab, and earn it on the existing relationship.

Sample script:

Since your auto is all set, can I do one quick thing for you? Bundling your home with it usually lowers both premiums and closes a gap most people do not realize they have. Worth two minutes to see your number?

Skills practiced: cross-selling, bundling value, relationship leverage.

Coaching takeaway: Practice framing the cross-sell as the customer's win, which is the difference between a trusted advisor and a product pusher.

An insurance sales roleplay scorecard you can use

Scenarios build skill only when the practice is scored, because a roleplay without a rubric is just a conversation. Use the scorecard below to grade any discovery, objection, or closing session consistently, whether a manager runs it or an AI platform scores it automatically.

What to score in an insurance roleplay

Score each dimension from 1 to 5, total it, and track the trend per agent over repeated sessions. The trend matters more than any single score, because steady improvement is the signal that practice is working.

Insurance roleplay prompts you can copy

Paste any of the prompts below into your AI roleplay tool or a general assistant to generate a realistic insurance scenario in seconds. Each prompt is written in clearly labeled sections so both the reader and the model know exactly how the customer should behave, including the compliance line the agent must respect.

1. Life insurance discovery prompt

This builds the needs-analysis conversation where the agent has to uncover the real need before recommending.

2. Premium objection prompt

This trains the agent to diagnose and reframe the most common objection in insurance without cutting coverage carelessly.

3. Closing prompt for a procrastinator

This builds the confident, honest close with a qualified prospect who keeps delaying.

Keeping insurance roleplay compliant

The feature that separates insurance roleplay from generic sales practice is compliance, and it is the one most scenario guides ignore.

Train compliant persuasion, not just persuasion

In a regulated sale, an agent who closes by promising a claim will be paid or by misstating coverage has created a liability, not a win. Insurance roleplay should reward the agents who sell persuasively while staying inside suitability rules, disclosure requirements, and product regulations, and it should flag the moments they overstep. Practicing compliant language under pressure is the only way it becomes automatic before a live, recorded, regulated call. Build the compliance checks into both the scenario and the scorecard so agents learn that selling and staying compliant are one skill, not two.

How to run and measure insurance roleplay

Good scenarios fail if the practice around them is rare, soft, or disconnected from real performance.

1. Run short, frequent, well-debriefed sessions

The most effective insurance teams practice in short bursts several times a week rather than in occasional marathon sessions, and they keep the focus to one skill at a time. After each run, give specific feedback tied to an observed behavior and its impact, then have the agent try it again, because the second attempt is where the skill actually sticks.

2. Measure what an insurance leader is judged on

Track close rate, objection-resolution rate, needs-analysis completeness, and renewal save rate for agents who practiced against those who did not, isolating the effect. The supporting evidence is strong, since companies that applied AI to sales coaching achieved3.3x higher growth in quota attainment, and in insurance the retention and compliance metrics matter just as much as new sales.

For multi-line agencies and carriers: scaling roleplay across the book

At agency and carrier scale, insurance roleplay has to cover many product lines, regions, and languages while staying consistent and compliant.

1. Build the family or committee decision, not one buyer

Many insurance decisions involve more than one person, a couple deciding on life coverage, or a business owner and a partner weighing commercial policies. Use multi-persona roleplay so agents practice aligning two decision-makers with different priorities, which is closer to how real policies actually get bought.

2. Standardize one compliant rubric across lines and states

Consistency is the agency-scale problem traditional coaching never solved. Define one governed scorecard that includes the compliance checks for each line and state, and run the practice in the languages your market speaks, so an agent in one region is held to the same standard as an agent in another.

3. Ground scenarios in your real recorded calls

Generic personas teach generic skills. Build AI customers from your real recorded calls and your own product and compliance documents, with customer data routed through proper privacy and protected-health-information handling, so the practice reflects your real book and your real regulatory environment.

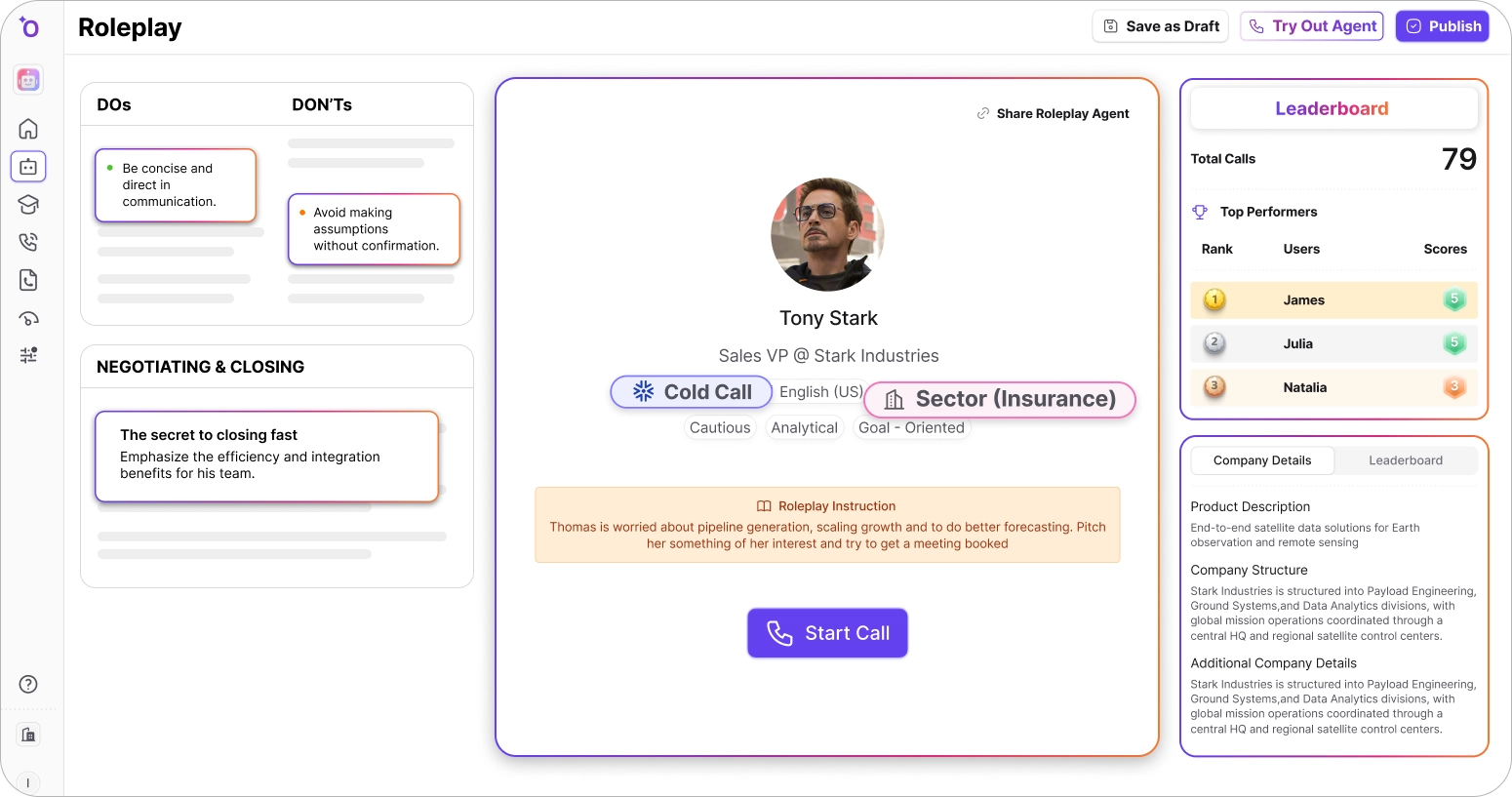

Here is how Outdoo AI builds insurance roleplay scenarios:

How Outdoo AI trains insurance sales teams

Outdoo AI is the enterprise AI roleplay and coaching platform built to run insurance sales training end to end, with the compliance posture a regulated industry requires.

1. Build insurance customers from your real calls and documents

Outdoo AI offers six ways tocreate a roleplay agent, so you can build a Medicare prospect from a real recorded call, generate a price-shopper from a prompt, or ground an agent in your product guides and compliance scripts so its objections and language match your actual market and rules.

2. Score discovery, objections, closing, and compliance

Every session is graded with a methodology-aligned or customscorecard you can build around needs discovery, objection diagnosis, value framing, the close, and compliant accuracy, so agents are scored on what earns and keeps a policyholder, consistently across the team and in 74+ languages for multilingual markets.

3. Practice high-volume objection handling and certify readiness

Agents drill objections in chat, voice, and video, and call-center teams run back-to-back reps throughCall Blitz, then certify readiness through courses with pass-fail gates before agents handle live customers. Completion exports to your learning system through SCORM and xAPI for the certification records insurance teams have to keep.

4. Close the loop on live calls, with a compliance-grade posture

Outdoo AI coaching scores real customer calls on the same rubric used in practice through Gong, Clari, and native conversation intelligence, then ties results to CRM data, so managers see whether the discipline agents built in practice shows up on live, recorded calls. For a regulated industry, the security posture matters as much as the scoring: Outdoo AI maintains SOC 2 Type 2, GDPR, HIPAA, and CCPA compliance with PII scrubbing, which is what makes it safe to practice health and Medicare conversations on real call data. Across the 15,000+ simulated conversations and 40 organizations inOutdoo AI's Readiness Report, agents who practiced more handled objections more consistently on live calls.

Make insurance roleplay a weekly habit

The insurance teams that win are not the ones with the best product manual, they are the ones whose agents have handled the hard moments so many times that empathy, compliance, and the close come automatically. Start with the single objection that stumps your team most, build a customer that pushes the way a real one does, score every session on discovery and compliance, and run it a few times a week.

Schedule a demo to see how Outdoo AI trains your insurance sales team across discovery, objection handling, and closing.

Frequently Asked Questions

.svg)

Insurance agents should practice across three pillars: needs discovery (life, Medicare, P&C needs analysis), objection handling (premium cost, existing coverage, rate increases, distrust), and closing (assumptive close, procrastinator urgency, cross-sell). Tailor each to the product line the agent sells.

AI roleplay gives agents unlimited, on-demand practice against realistic objections like price, existing coverage, and distrust, with instant scored feedback. Repetition turns calm, compliant responses into a reflex under emotional pressure.

Build the compliance line into both the scenario and the scorecard, so agents are flagged when they promise a claim outcome, misstate coverage, or recommend an unsuitable product. Practicing compliant language under pressure is the only way it becomes automatic.

Yes. Strong platforms let you build product-specific personas and scenarios for life, health, Medicare, P&C, and commercial insurance, each with the objections, communication style, and compliance rules of that line.

AI roleplay does not replace manager coaching. It handles unlimited repetition and consistent, compliant scoring at scale, while managers add strategic and relationship coaching only a human can.